Most "R&D tax credit" claims I get asked to look at in construction don’t qualify. Not because contractors aren’t doing clever work — many are — but because clever isn’t the test. The test is whether you faced a genuine scientific or technological uncertainty that a competent professional in your field couldn’t have just looked up. The merged RDEC scheme, in for accounting periods starting on or after 1 April 2024, has tightened both the qualifying rules and the paperwork. This is the filter I run for Yorkshire contractors before they spend a penny with a claims specialist.

QUICK ANSWER

The merged RDEC scheme gives Ltd companies a 20% above-the-line credit on qualifying R&D — worth roughly 15–16p in the pound after corporation tax. In construction, qualifying work is narrower than R&D mills suggest: modular building methods, retrofit problem-solving, bespoke engineering, and novel M&E systems. Miss the pre-notification deadline or skip the Additional Information Form and your claim is invalid, full stop.

The two questions HMRC actually asks

HMRC doesn’t care that your project was difficult, expensive or under time pressure. It cares about two questions, both lifted from the 2023 DSIT Guidelines on the meaning of R&D for tax purposes.

Question one: did the project seek an advance in science or technology? The advance has to be in overall knowledge or capability in a field of science or technology. Not your own knowledge — the field’s. If a competent in-house engineer or a specialist sub could have figured it out from publicly available information, codes of practice or a manufacturer phone call, it’s not an advance.

It’s just work you hadn’t done before. "We hadn’t built one of these before" isn’t R&D. "Nobody in the industry had a reliable way to make this work without spending six figures on prototypes" might be.

Question two: did you face genuine scientific or technological uncertainty? Not commercial uncertainty (we didn’t know if we’d make money). Not procurement uncertainty (we couldn’t get materials). Not regulatory uncertainty (we weren’t sure planning would approve). Uncertainty about whether the technical objective could be achieved, and how.

The yardstick is whether a competent professional in your field could have resolved it from existing knowledge. If yes, no uncertainty. If they’d have had to investigate, test, redesign or model their way to an answer, yes.

Pass both questions and there’s likely a claim worth pursuing. Fail either, and there isn’t.

What qualifies in construction — and what genuinely doesn’t

Four areas regularly hold up to the DSIT tests in my scoping calls:

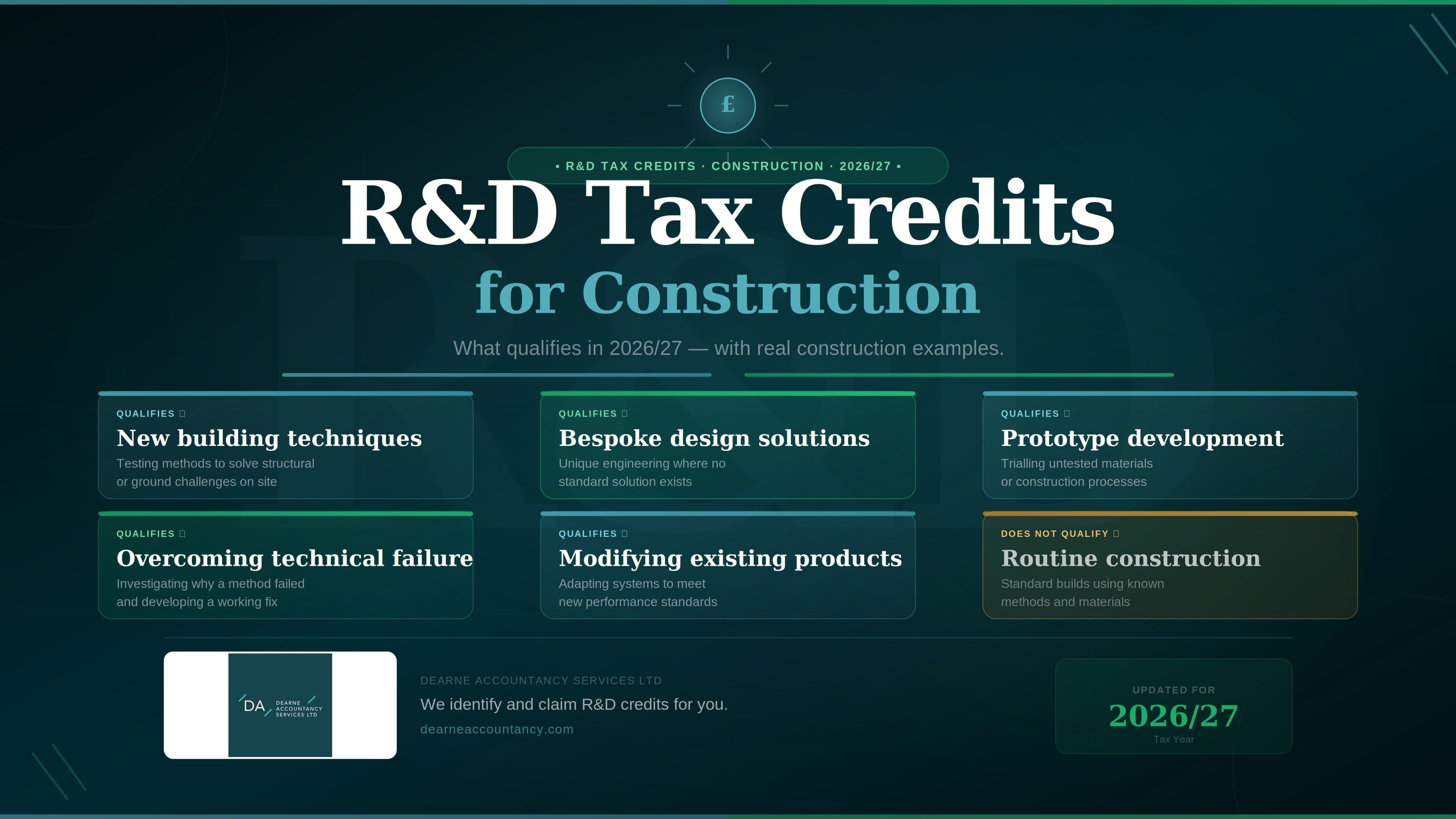

1. Modern Methods of Construction (MMC). Modular, volumetric, panelised and offsite work. The uncertainty isn’t usually "can we build it" — it’s whether a particular system performs structurally, thermally or acoustically when adapted to a non-standard plot, joint detail or load condition. Bespoke jointing for SIPs panels. Hybrid CLT-and-steel structures with load paths the standard guidance doesn’t cover. Novel waterproofing details on modular pods.

2. Retrofit and sustainability. The fastest-growing qualifying area I see. Fabric-first retrofits on awkward stock — Victorian terraces, listed buildings, mixed-construction industrial estates — throw up problems standard solutions can’t touch without causing interstitial condensation, thermal bridging or fabric damage.

Novel low-carbon concrete mixes for specific site conditions. Passive ventilation systems retrofitted into deep-plan buildings. PV integration into structurally limited roofs.

3. Site-specific structural and geotechnical engineering. Non-standard ground conditions are the most common trigger. Bespoke piling design where standard methods failed. Contaminated land remediation needing novel containment.

Basement waterproofing in high water-table conditions. Complex temporary works on confined sites. Standard codes cover most cases. When they don’t and your team had to develop a solution iteratively, that’s the territory.

4. Bespoke M&E and building services. Heat-recovery systems for industrial processes. Renewables integration into older buildings. District heating or off-grid designs. Bespoke HVAC in food processing, clean rooms or listed properties. The uncertainty sits around integration, performance under non-standard load profiles, or interaction with existing systems.

What does not qualify — and this is where R&D mills will tell you otherwise:

- Standard build-to-spec, even on a complex job. Difficulty isn’t uncertainty.

- Routine value engineering or cost optimisation. Saving money is commercial, not technical.

- Aesthetic design, planning input, client liaison.

- Project management improvements — new software, scheduling, lean processes.

- Following published codes, BBA certificates or manufacturer guidance, even on a tricky build.

- Adapting an existing technique to a new site where the answer was knowable up-front.

If your project is genuinely none of the above, there’s likely a claim. If it’s mostly the above with some technical content sprinkled in, the honest answer is no.

The merged RDEC scheme in 2026/27 — how the maths actually works

For accounting periods starting on or after 1 April 2024, there’s one mainstream scheme: the merged RDEC. It replaced the old SME relief and the original RDEC. One regime, one rate, one set of rules, regardless of company size (with one exception covered in the next section).

The headline rate is 20% of your qualifying R&D expenditure, applied as an above-the-line credit. The credit goes through your profit and loss as taxable trading income, then either reduces your corporation tax bill or, where it can’t, gets paid out in cash through a set of priority rules.

Because the credit is taxable, the net benefit depends on your tax position:

| Your position | Qualifying R&D | Gross credit (20%) | Tax on credit | Net cash benefit |

|---|---|---|---|---|

| Profit-making, small profits rate (19%) | £100,000 | £20,000 | £3,800 | £16,200 |

| Profit-making, main rate (25%) | £100,000 | £20,000 | £5,000 | £15,000 |

| Loss-making | £100,000 | £20,000 | £3,800 (notional, at 19%) | £16,200 |

Plan on roughly 15–16p in the pound of qualifying spend, before fees. That’s the figure to anchor any conversation around — not the headline 20%.

A few practical points worth flagging. The PAYE/NIC cap caps payable credit at £20,000 plus three times your relevant PAYE and Class 1 NIC liabilities for the period. Most contractors with reasonable payroll are nowhere near it; specialist subs with small payroll and heavy subcontractor spend can hit it.

Excess carries forward. The trading requirement means you need to be trading and chargeable to corporation tax — sole traders, partnerships and LLPs without a corporate member cannot claim. Subcontractor spend qualifies up to 65% of unconnected-party invoices, with the contracted-out rules below dictating who actually claims.

ERIS — the route for loss-making R&D-intensive SMEs

There’s one carve-out from the merged scheme. Loss-making SMEs with R&D-intensive operations can choose Enhanced R&D Intensive Support (ERIS) instead. The eligibility test has two parts:

- SME size: fewer than 500 staff and either turnover under €100m or balance sheet under €86m.

- R&D-intensive: qualifying R&D expenditure is at least 30% of your total tax-deductible expenditure for the period (down from 40% in periods starting before 1 April 2024).

A "year of grace" rule helps if intensity dips: if you met the 30% test in your prior 12-month period and filed a valid claim, you can still claim ERIS in a period where intensity falls below 30%.

The mechanics differ from the merged scheme:

| Step | Mechanism | Effect on £100k qualifying spend |

|---|---|---|

| 1. Enhanced deduction | 86% additional on top of the normal 100% | £186,000 total deduction |

| 2. Surrender the loss | Surrender up to the enhanced loss for cash | up to £186,000 surrenderable |

| 3. Payable credit | 14.5% of the surrendered loss | up to £26,970 cash |

ERIS can deliver up to roughly 27p in the pound — meaningfully more than the merged scheme’s 15–16p — but only for firms that genuinely meet the intensity test. In construction that’s usually early-stage MMC firms scaling pre-profit, sustainability-focused specialists with concentrated technical headcount, and some retrofit start-ups. Established contractors with broad commercial overhead won’t get there.

Who actually claims — the new contracted-out R&D rules

This is the change most contractors haven’t fully absorbed. Under the old SME scheme, a subcontractor doing R&D for a main contractor generally couldn’t claim, and the customer often couldn’t either. Lots of genuine R&D fell into the gap.

The merged scheme uses a different test, in CTA09/S1133. HMRC asks who decided the R&D should be done — who "intended or contemplated" that R&D of that kind would happen when the contract was signed. "Intended or contemplated" means more than knowing R&D might happen.

It means the customer specifically appreciated what R&D would be done and why. Boilerplate clauses won’t get you over the line.

In practice on a typical construction project:

- Main contractor signs design-and-build with the client. The client is usually not intending or contemplating R&D. The main contractor takes the claim where they bear the technical risk.

- Main contractor engages a structural engineer on novel ground conditions. If the main contractor specifically asked the engineer to develop a bespoke design, the main contractor claims for the engineer’s qualifying time. The engineer doesn’t.

- Specialist sub brought in for a standard scope, encounters R&D in delivery. If the main contractor didn’t intend R&D up-front, the subcontractor likely owns the claim — they’re doing it on their own initiative.

Get this wrong and you’ll have two parties claiming the same costs, or both walking away. Worth scoping before the first invoice goes out.

The two compliance gates everyone trips over

The maths is one thing. The paperwork has killed more valid claims in the last two years than HMRC enquiries ever did.

Gate one: the Claim Notification Form (CNF). For periods of account starting on or after 1 April 2023, you have to pre-notify HMRC if you’ve never claimed R&D before, or your last claim was made more than three years before the end of the current notification period. The window runs from the first day of the period of account to six months after period end.

So a 31 March 2027 year-end has a CNF deadline of 30 September 2027. Miss it and the claim is invalid — no extension, no appeal. I see this catch contractors out twice a month. A first-time claimant works through 2026 thinking they’ll deal with R&D when the tax return goes in, and by the time the accountant flags it, the CNF window has shut. The relief is gone.

Gate two: the Additional Information Form (AIF). Mandatory for every R&D claim submitted from 8 August 2023 onwards. You file it before (or with) the CT600.

It requires the senior R&D contact, accounting period, project descriptions tied to the DSIT framework (advance sought, uncertainty faced, baseline knowledge, resolution approach), and a breakdown of qualifying expenditure by category.

No AIF, no claim. If the AIF arrives after the CT600, HMRC removes the R&D claim from the return.

Time limit overall. Two years from the end of the period of account, under Schedule 18 paragraph 83E of Finance Act 1998. A 31 March 2025 year-end needs the claim filed by 31 March 2027. The CNF window usually binds tighter, so don’t rely on the 2-year clock.

Worked examples: four Yorkshire firm types

Each is illustrative — composites built from typical scenarios I see, not specific clients. Numbers are indicative; real claims need full scoping.

Example 1: Barnsley MMC housebuilder, year-end March 2027. Building 80 timber-frame homes a year using a SIPs panel system. On a sloped, narrow plot in 2026, the standard panel-jointing detail wouldn’t sit within tolerance with the foundation design.

The technical lead spent six weeks developing and testing a modified joint with the panel manufacturer’s engineer, validating structural performance and thermal continuity.

- Qualifying: joint development time, the engineer’s hours, prototype materials, testing.

- Not qualifying: the rest of the build, the standard panels, marketing, sales.

- Indicative spend: £35k qualifying. Profit-making → merged RDEC. Net ~£5,700. CNF needed if first claim.

Example 2: Sheffield retrofit specialist, year-end September 2026. Fabric-first thermal upgrades on Victorian terraces, EnerPHit-targeting. Standard external wall insulation caused interstitial condensation modelling failures because of the parging coat under the original brick.

The team designed a hybrid detail (modified internal + targeted external work) and validated it with hygrothermal modelling and on-site sensors before rolling out across the terrace.

- Qualifying: design, modelling, sensor monitoring, the iterative redesign.

- Not qualifying: standard EWI installation on the remainder.

- Indicative spend: £58k. Loss-making, low intensity → merged RDEC. Net ~£9,400 as cash.

Example 3: Doncaster M&E contractor, year-end December 2026. Bespoke heat-recovery and humidity-control for a food-processing facility expanding into a new product line. Packaged off-the-shelf units couldn’t handle the required temperature differentials without condensation.

The team designed a custom configuration, modelled airflow, and ran a four-week commissioning programme to tune it.

- Qualifying: design engineering, modelling, commissioning iteration.

- Not qualifying: standard ductwork, fan installation, off-the-shelf controls used as supplied.

- Indicative spend: £42k. Profit-making → merged RDEC. Net ~£6,800.

Example 4: Rotherham civils firm, year-end June 2026. Brownfield groundworks where standard CFA piling failed due to contaminated made-ground over a shallow watercourse. The team developed a sleeved-pile design with bespoke grout mix, working with the geotech consultant. Two weeks of redesign, three test piles before sign-off.

- Qualifying: geotech consultant hours, redesign time, test pile materials and installation.

- Not qualifying: the rest of the piling, muck-away, standard reinforcement.

- Indicative spend: £48k. R&D-intensive small firm in a loss period → ERIS. Net ~£12,900 cash credit.

Why R&D mills are dangerous (and what good looks like)

I’ll tell you honestly. The R&D claims market has a hygiene problem.

The cold callers offering "100% success, no win no fee, we’ll find a claim in any business" are not your friends. HMRC enquiry rates on construction R&D claims have climbed sharply since 2023, and the Random Enquiry Programme means even small claims can be reviewed.

When a mill recycles the same technical narrative across thirty clients with different work, that’s the first thing an inspector spots.

The cost of getting it wrong is more than losing the claim:

- Repayment of the credit, plus interest.

- Penalties — up to 100% of the tax under-declared in deliberate cases.

- A flag on your file that affects future claims.

- Director-level enquiries where HMRC suspects deliberate behaviour.

What good R&D scoping looks like. A technical narrative written from your project, with your competent professional’s input, not boilerplate. Time and cost records that tie expenditure to qualifying activities — not a blanket "20% of everyone’s time on R&D" estimate.

CNF filed inside the window if needed. AIF aligned with the CT600. An accountant or specialist who can show you previous successful claims in your sector and answer detailed questions about your work.

How we work at Dearne. I’ll scope the claim with you on a 30-minute call. Honest answer either way.

If it qualifies, I’ll explain what good evidence looks like and refer you to an R&D specialist we trust to prepare the formal claim — and stay in the loop so the corporation-tax mechanics flow back into your books cleanly.

If it doesn’t, I’ll tell you before you spend money on it. That’s not a feature I charge extra for. It’s the bare minimum.

Frequently asked questions

Can I claim R&D credits if I’m a CIS subcontractor working through my own Ltd Co?

Yes, if your Ltd is paying corporation tax and the technical work passes the DSIT tests. CIS is how tax is collected on your invoices — it doesn’t affect R&D eligibility on the corporation-tax side. The work itself needs to qualify, not your CIS status. For the Ltd-co side of CIS, see our guide to claiming back CIS suffered as a limited company.

How far back can I claim?

Two years from the end of the period of account, under Sch 18 para 83E FA 1998. A 31 March 2025 year-end needs the claim filed by 31 March 2027. If it’s a first claim, the CNF deadline (six months after period end) will usually bind tighter.

The project finished last year. Is it too late?

Maybe not — check the CNF clock first. If you’ve claimed R&D in the last three years, you don’t need a CNF and the standard 2-year claim window applies. If you’ve never claimed, the CNF deadline is six months after the period-end the spend fell in. If that’s passed, the relief is gone.

We use Polish welders on a few site shifts. Does our overseas spend qualify?

Almost certainly no, post-April 2024. Overseas EPW and subcontractor spend only qualifies where the activity necessarily takes place abroad for geographical, environmental, social or regulatory reasons. Cost and worker availability are explicitly excluded. UK-based site activity using overseas-payrolled workers won’t get past it.

We’re a sole trader / partnership. Can we claim?

No. R&D tax credits are corporation-tax relief. You’d need to be a Ltd company, or have a corporate partner in the case of a partnership. If you’re considering incorporation, the R&D piece is worth weighing — but it can’t backdate.

Let’s see if you’ve got a claim worth pursuing

If you think your construction work might qualify, talk to me before you talk to a claims firm. I’ll spend 30 minutes scoping it honestly. If there’s a claim worth pursuing, I’ll point you at a specialist I trust. If there isn’t, I’ll save you the fee. Book a scoping call.

Looking for the wider picture on construction tax and compliance? Start with our Construction Accountants hub, or read the Domestic Reverse Charge pillar guide for the VAT side of the same client base.

Sources & further reading

GOV.UK: The merged R&D scheme and Enhanced R&D Intensive Support

HMRC: CIRD115000 — New RDEC rates

HMRC: CIRD121000 — ERIS overview · CIRD122000 — ERIS calculation · CIRD123000 — R&D intensity condition

HMRC: CIRD161000 — Contracted-out R&D

HMRC: CIRD150500 — Overseas restrictions overview

HMRC: CIRD81300 — Definition of R&D

HMRC: CIRD183000 — Pre-notification of claims

GOV.UK: Submit detailed information before you claim R&D tax relief (AIF)

GOV.UK: Tell HMRC you’re planning to claim R&D tax relief (CNF)